Creating a new market involves more than just developing a new product or service; it requires convincing the majority to see the world differently.

For many entrepreneurs, the opportunity to pioneer a new market and build a successful business from scratch is incredibly exhilarating, and the pinnacle of intellectual and industrial innovation.

Vision plays a central role in this process, yet it must be paired with reality.

Companies and teams that successfully create new markets can dominate and experience rapid revenue growth, enhanced brand reputation and the pleasure of being the first to figure out something truly new.

The Joy Of Creating New Markets

The prospect of creating new markets is enticing because it represents an opportunity to make a meaningful dent in the universe.

Introducing new products or services to the market can have a significant impact on people's lives, societies, and the economy as a whole.

We celebrate the insights that drove leaders from Estée Lauder to Jeff Bezos to see a different perspective, and create worlds we now take for granted.

Whether it's improving efficiency, enhancing convenience, or addressing social and environmental challenges, creating new markets allows businesses and entrepreneurs to make a lasting, positive difference in the world.

The Importance Of Creating New Markets

Creative destruction is a concept introduced by economist Joseph Schumpeter to describe the dynamic process where new innovations continuously replace older ones, leading to the destruction of existing products, industries, or ways of doing what we do.

This process is “creative” because it generates new products, services, industries, and jobs, often bringing about higher productivity and economic growth.

However, it's also “destructive” because it inevitably leads to the decline or obsolescence of existing firms, technologies, and practices.

As cars replaced horses, and later flipped from individual ownership to shared mobility services like car-, bike-, and scooter-sharing, transforming urban transportation. These shifts can be game-changing and challenging.

That said, creating new markets ultimately paves the way for progress, driving economic advancement and changes in customer behavior.

What To Unlearn When Creating New Markets

For many when they hear about creating new markets, they still think of creating a better product or service.

Yes, being cheaper, better and faster than the competition is part of it but that’s only one piece of the puzzle.

Similarly, blindly deploying new technology without crisp customer need is a mug's game—yes I’m looking at the hundreds of “web3 versions of Airbnb” with no differentiated use case.

The real trick to creating new markets is to give people superpowers they never had, thought or believed possible before.

For example, home owners didn’t realize they could be hosts and create additional wealth before AirBnB. The majority's reaction to the initial concept was “that’s weird”.

Telling people strangers driving them around would be the norm in the early days of Uber triggered the same response. Similarly, who thought people would want to make a few dollars extra, giving people they never met before a ride home on their commute?

Novel innovations create new markets by creating agency for customers in ways never before possible. It often challenges the identity of customers themselves, always their expectations or the role they can play in performing desired tasks.

This is what new market creators thrive on. Seeing the future, recognizing the inflection points in technology, regulatory, user needs or emerging trends that give customers new superpowers, and turn into monster businesses over time.

So how do you do it? What mistakes should you avoid?

Challenges and Shifts In Creating New Markets

Creating new markets can be an exhilarating yet daunting endeavor. Here are some challenges you might face:

Identifying a Niche: Tesla identified a niche in the automotive market for electric vehicles with high performance and sleek design. The secret was selling high-end cars to high-paid people. By focusing on this segment, they were able to differentiate themselves from traditional automakers and make electric cars cool.

Educating Consumers: When Airbnb first launched, they faced the challenge of convincing travelers to stay in strangers' homes rather than hotels. Through clever marketing campaigns and user testimonials, they educated consumers about the benefits of a more personalized and affordable accommodation experience.

Regulatory Hurdles: The ride-hailing company Uber faced regulatory challenges in many cities due to resistance from traditional taxi industries and concerns about safety and employment practices. They had to navigate complex regulatory landscapes and engage in dialogue with policymakers to operate legally in various markets.

Cultural Differences: McDonald's had to adapt its menu and marketing strategies to suit local tastes and preferences when expanding into international markets. For example, they offer different menu items in India to accommodate cultural dietary preferences and religious beliefs. It even gave rise to tourists traveling the world to try each unique meal on the menus.

Knowing the obvious challenges helps, yet how to make sure you create new markets correctly?

Frame The Opportunity Then Flip Customer Behavior

Let's start by examining the mindset that Jack Dorsey when founding Square, now rebranded as Block, a corporation valued at $70 billion.

This initiative revolutionized the market for credit card readers, particularly benefiting individuals and microbusinesses like farmers’ market vendors, food trucks, and pop-up shops, which previously struggled to accept credit card payments—while also winning a device design award along the way.

The inspiration stemmed from witnessing his future co-founder, Jim McKelvey, lose a sale of hand-blown glass due to limited credit card acceptance capabilities. Recognizing the potential loss in impulse purchases, they delved deeper into the issue.

They discovered a widespread desire among people to use credit or debit cards for small transactions, yet existing credit card payment systems were inaccessible to most individuals and microbusinesses. These systems, dominated by well-established players catering to large retailers, were expensive, complex, and cumbersome, posing significant barriers to entry.

Framing that opportunity and refusing to accept this status quo, Dorsey and McKelvey envisioned a future where no individual or small business would lose sales due to an inability to accept credit card payments. Thus, they developed the Square Reader, a simple device that plugs into a mobile phone, making it convenient and portable.

With a pay-as-you-go model, where retailers only pay when they use the device, Square appealed to small businesses, pop-up shops, and even individual transactions like those involving babysitters, ice cream trucks, and local builders.

Remarkably, Square's innovation didn't disrupt existing merchants and credit card providers to a significant extent. It gave individuals and microbusinesses the superpower to process micro transactions—eventually expanding into tools to manage their business, financial reports, launch websites and loyalty programs.

Square swiftly ascended to become a billion-dollar company without facing substantial resistance from established players because they created a new market.

If you haven’t, listen to my UNLEARN podcast with Jim McKelvey, in which we dive into their story in greater detail. Leave a review too.

Technology Is Not The Answer. It’s The Enabler

Nowadays, it is easy to be seduced by technology. Too many companies and startup founders see technology innovation as the path to market creation. They focus on how to shoehorn the latest technologies into new market offerings they hope will take off—I’m looking at you now AI companies! (whatever they are).

Teams get burned when the market they’re aiming to create doesn’t materialize because people—plain and simple—are not convinced of the value it will deliver to them. They confuse the means with the ends, and miss the mark.

The trick is to see technology as the great enabler not the answer to realizing value. Technology enables products to be cheaper, faster, better. Offering customers a leap in value is what ultimately creates a new market, not a technological bumper sticker.

One great example of technology enabling market creation is Evalify, a revolutionary platform that allows investors to streamline the process of evaluating startups by using intellectual property, particularly patents, as a benchmark to assess the potential and originality of early-stage ideas from just uploading a pitch deck.

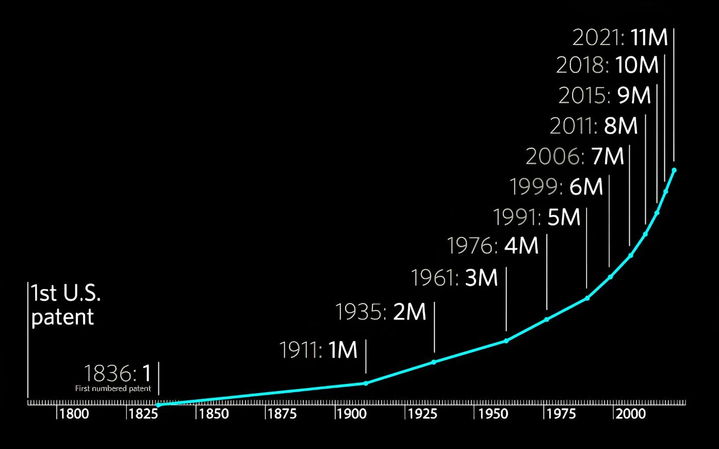

Reference: https://www.uspto.gov/patents/milestones

Consider this: it took the United States Patent and Trademark Office 75 years to issue its first million utility patents, then 14 years to move from the 4 millionth to the 5 millionth patent between 1976 and 1991, and just 35 months to progress from the 10 millionth to the 11 millionth (between 2018 and 2021).

This acceleration in patent filings reflects a landscape where innovation moves at breakneck speeds, turning the business environment into a “crowded square” filled with potential conflicts and opportunities.

The pace at which new patents are filed means that yesterday’s clear paths may be today’s legal entanglements. For investors, this isn’t just about avoiding pitfalls; it’s about seizing opportunities that others might miss because they are not looking deeply enough into the IP landscape.

To date, innovators to investors haven’t thought of asking hard questions like how patentable this idea is, or are there any IP impacts to this idea? The simple thought of such questions leads directly to responses such as, “that’s too expensive, takes too long and has too limited a scope for a lawyer to provide a confident answer”. Therefore, only in extreme cases and often after hours of investment of time, energy and money might investors consider such questions or it a task worth doing.

No more. In minutes, at a fraction of the cost, covering almost 200,000,000 patent documents across industries from any language and 170+ countries or jurisdictions, Evalfiy gives investors feedback, guidance, and insights on relevant patents they must be aware of and IP-derived opportunities, issues, and with freedom to operate in the space the startup has decided to plant their flag.

This isn’t just a new tool. It’s a new mindset and market created by what technologies such as cloud computing, machine learning, and data model processing have enabled—and it’s only the beginning.

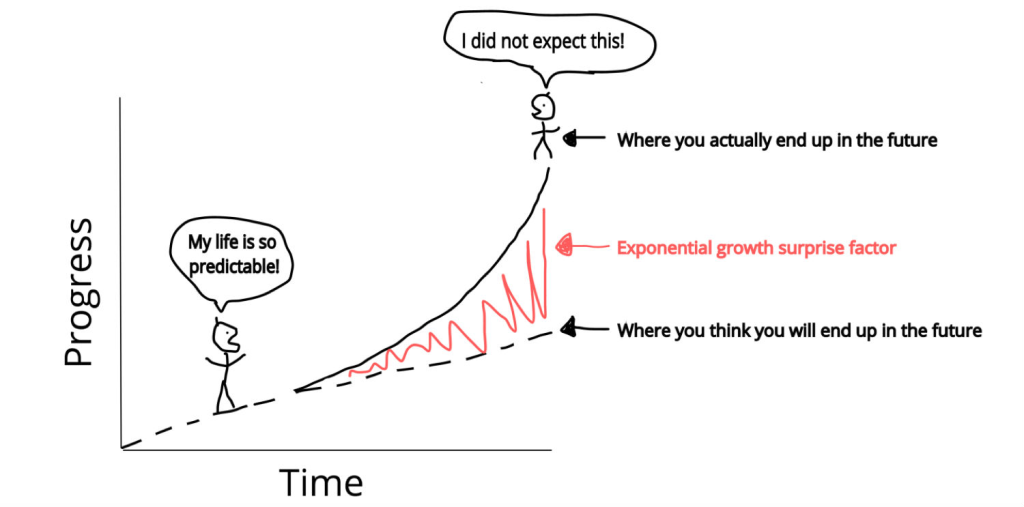

One of the visualizations we use a lot about at Singularity University where I’m faculty is exponential technology, and innovation curvers. The most fascinating part of exponential innovation curves is how deceptive they appear.

In the early stages of an exponential curve, there's often a lot of hype and excitement surrounding the technology or innovation.

Exponential curves typically start with a period of slow growth that can be deceiving; it seems like the technology or innovation isn't making much progress. Yet, once an exponential curve reaches a certain tipping point, the rate of growth can accelerate rapidly, catching many off guard.

People tend to have difficulty grasping the full extent of exponential growth, especially when it involves technologies or concepts that are outside their area of expertise or go against norms.

I’ve seen it time and time again during my career.

Why would you build a mobile app over a website? Boom! Hello iPhone.

Why would you put your infrastructure in the cloud over a physical server? Boom! Hello AWS.

Why would you check the patents relevant to your idea in the earliest stages? It’s too expensive, too slow, and only covers a small domain the lawyer can read, and understand. Boom! Hello Evalify.

Deception of Linear vs Exponential Curve

Exponential innovation curves offer tremendous opportunities for progress and advancement, they can also be deceptive and require a small set of customers to see the vision, experience the new superpower and ride the wave as it goes exponential.

Evalify is a new digital compass for the modern investor. In today’s crowded square of ≈200M+ patent documents globally to date and growing exponentially, Evalify is your strategic advantage, illuminating paths that many don’t even know exist.

It’s time to change and rethink early-stage decision-making for good.

Timing Is An Art

The final piece worth noting is the most elusive of all: timing.

Timing is critical in market creation, with entrepreneurs needing to align their vision with emerging trends and technological advancements. The ability to adapt and pivot in response to market dynamics is essential for success.

In fact, co-founders of Evalify, William and Nick mention how the perfect storm of technology advancements, digitalization of patents, and the power of data processing and modeling has been the key inflection point in making Evalify’s hard-to-copy capabilities get exponentially better.

You can be too early. You can be too late. Yet nothing beats being on time. The magic of catching a wave in shifts in technology, regulations, customer needs or emerging trends is a powerful force. Yet the hardest to anticipate. It's continuously making bets, seeking out inflection moments, and being ready to respond when they happen.

Getting Started Creating New Markets

While creating new markets is fun, failure is just as common in entrepreneurial ventures.

Always remind yourself that each effort contributes to personal growth and development, making purposeful risk-taking a valuable exercise for personal growth, intellect and human capital.

Market creators lead with agency and give customers new superpowers they have had before.

Rather than starting with what exists today, they envision what could and should be, irrespective of what is.

They flip the script, openly questioning and reimagining what superpowers might be missing.

They ask: Why not? What if? That allows them to see what others can’t see, to question what others don’t question, and to reinterpret what is possible and how to achieve it.

Ask your team (and yourself):

- Are we prioritizing rigid structures and old systems over our ability to give customer agency?

- Do we default to technological solutions, or do we prioritize creating tangible value for our users?

- Are we limiting ourselves by seeking solutions from a select few, or are we harnessing the collective creativity of our entire team or our crowd, as we do at Nobody Studios?

- How can we foster a culture that encourages curiosity and exploration?

- Are we focused on merely sustaining existing markets, or are we actively seeking to create new ones?

These questions, along with embracing diverse perspectives, serve as a guiding compass in cultivating a culture of creativity essential for fostering market-creating innovation.

They exert a powerful influence on your conversations, expectations, and behavior, and help establish a culture of creativity that is fundamental to generating market-creating innovation.

ABOUT THE AUTHOR

Barry O'Reilly

Co-Founder + Chief Incubation Officer of Nobody Studios

Barry is an entrepreneur, business advisor and author who has pioneered the intersection of business model innovation, product development, organizational design, and culture transformation.

1 Comment

Pingbacks

-

[…] example, Barry O Reilly, Chief Incubation Officer at Nobody Studios, highlights that creating new markets can be an exhilarating yet daunting endeavor. Typical challenges include […]

[…] example, Barry O Reilly, Chief Incubation Officer at Nobody Studios, highlights that creating new markets can be an exhilarating yet daunting endeavor. Typical challenges include […]

{kind=link}